I have a confession to make: I used to disregard the RSUs part of my compensation. It’s not “real” money coming into my checking account, so it doesn’t count. Recently, I decided to learn more about personal finances and gained a new appreciation for them!

Unfortunately, the stock portion of your compensation is not straightforward: RSUs vs shares, vesting options, taxed once, taxed twice…With all that, how much money do you end up with? This is a complex calculation, that I’m here to help with!

We’ll start with some general information, and then go through a real-life example!

Of course, nothing here is financial advice. I’m a software developer, not an accountant. Also, let me clarify — I am only using information available on the internet.

What are RSUs?

RSUs are Restricted Stock Units and are a common part of the employee’s compensation. They are called restricted because it is not fully transferable until certain conditions have been met (like tenure).

RSUs are a retention tool for employers: The employees have an incentive to stay in the company longer until the next RSUs are vested.. and the next ones.. and the next ones. Also, the employee might perform better knowing the success of the company will lead to an increase in share value, which will be worth more money for them (compared to a fixed base salary that will come in regardless of the company’s performance).

RSUs have a life cycle: First, they are granted to you (saved for you, kind of like a reserved table at a restaurant), and when the time comes — they are vested: The shares are yours! But… don’t get too comfortable, because you need to pay taxes on that income!

(Note that I use the words “share” and “stock” to describe the same thing, but if you want to be precise – “stock” is the financial instrument a company issues, and a “share” is a single instance of that financial instrument. — source)

Vesting Options

When it comes to vesting, there are three routes you can go: Selling all the new stocks (sell-for-profit), selling just enough to cover their taxes (sell-to-cover), or paying the taxes in advance (which are 52.1% today in Ireland). The choice depends on how much cash you can/will invest in it and whether you think the stock will increase in value. Some might prefer cashing the stocks and investing in other things by themselves. The default is sell-to-cover.

Lastly, if you choose to keep some stocks and they gain profit— once you sell them — you need to pay the capital gain tax of 33% (yes, EVERYTHING is taxed).

Share split

At some point, a company might decide to split the shares into smaller shares. In Amazon’s case, if you had a single share with a value of $3200 before the split— after the split you’ll own 20 shares of $160, which totals the same amount. That way, the shares are more affordable.

If you check the history of a certain stock online, you will see only the new (smaller) value —which can confuse you when you check the history of your RSUs. Don’t worry, it will be clearer with a real-life example!

Brokerage account

A brokerage account allows one to invest in publicly traded assets such as stocks. You probably can choose between brokerage companies your employer works with. Once you set up your vesting preferences, they will do the rest.

There are two fees you should be aware of: The first is the Trading Commission, which anyone who trades pays, regardless of which broker they choose to go with. The second one is the Supplemental Transaction Fee, which is an additional fee you pay your broker.

All the calculations we will see today do not include those fees.

Real Life Example

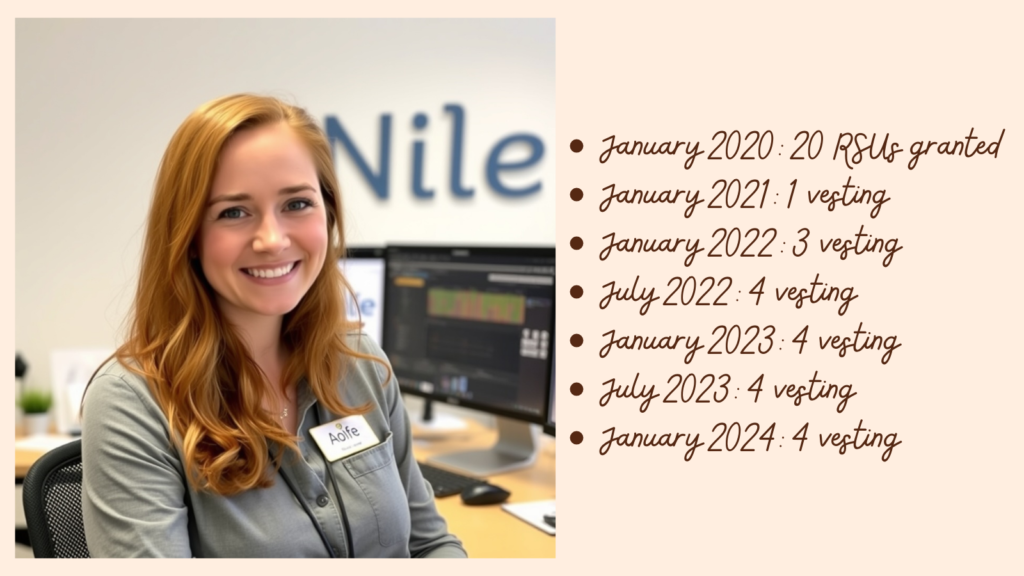

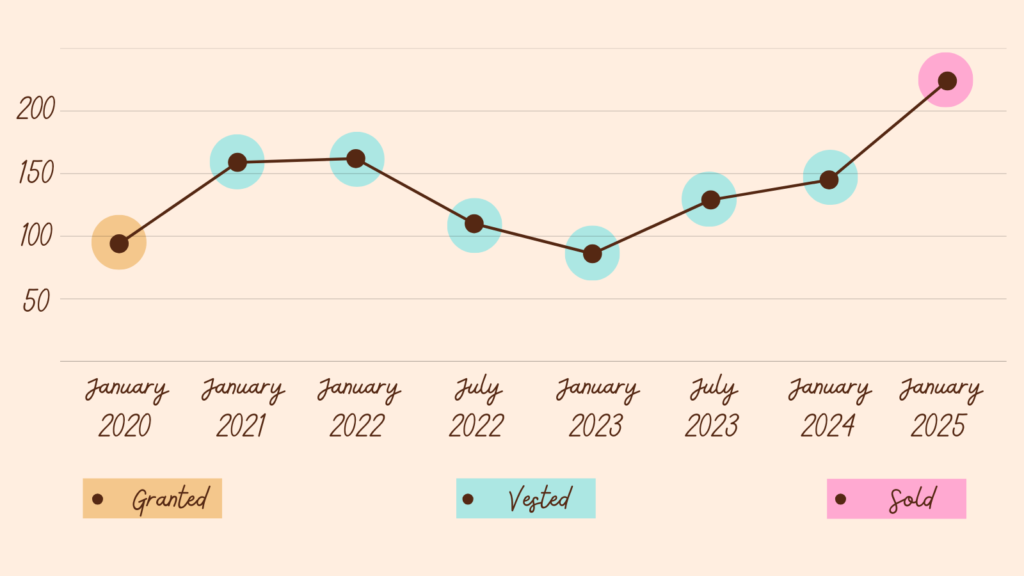

Meet my AI-generated friend, Aoife. She started working in a company called Nile 5 years ago (in January 2020). Her vesting approach from the beginning was to sell-to-cover. Let’s help her calculate the “real money” that will come out from the RSUs granted upon signing the contract if she were to sell them today (in 2025).

Aoife signed a compensation plan containing 20 RSUs, and her employment started in January. In her contract, it says that “RSUs follow a 4-year vesting schedule: 5% on the 15th day of the month in which you reach your first anniversary of employment, 15% on the 15th day of the month in which you reach your second anniversary of employment, and 20% every six months thereafter, until fully vested.”

Therefore, in Aoife’s case:

*Note that Amazon’s RSUs (Oops! Nile’s RSUs, I mean) went through a 1 to 20 split in June 2022, which will make our calculation even more complex!

Now, let’s add the value of the stock at the time to each line. I’ll be rounding the values for easy calculation, but you can see the exact share value in your periodic stock documents. Note that the value is post-split!

Here are the numbers we are working with:

RSUs granted:

January 2021: 1 (=20) RSU, share value: $160

January 2022: 3 (=60) RSUs, share value: $162

July 2022: 4 (=80) RSUs, share value: $110

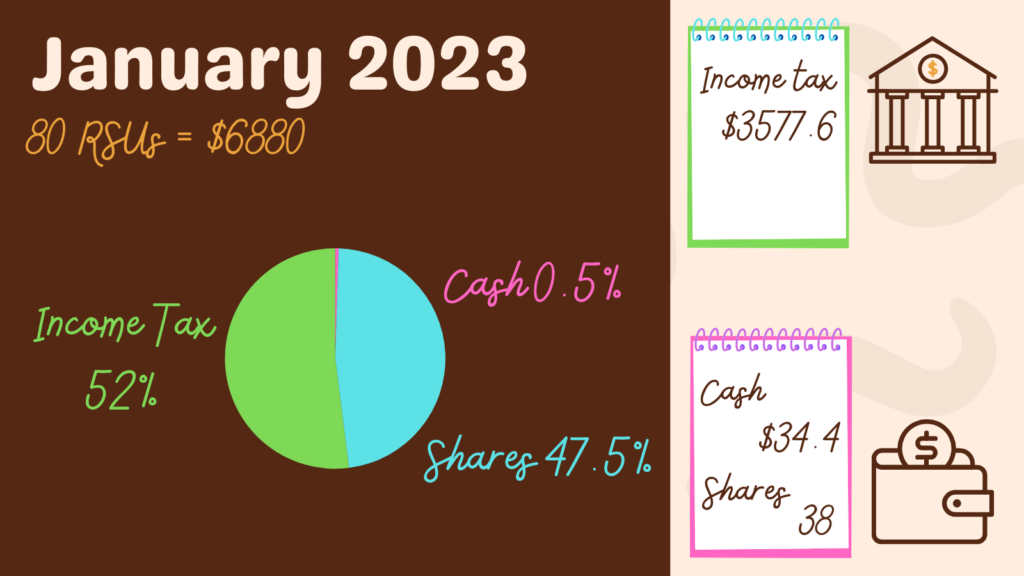

January 2023: 4 (=80) RSUs, share value: $86

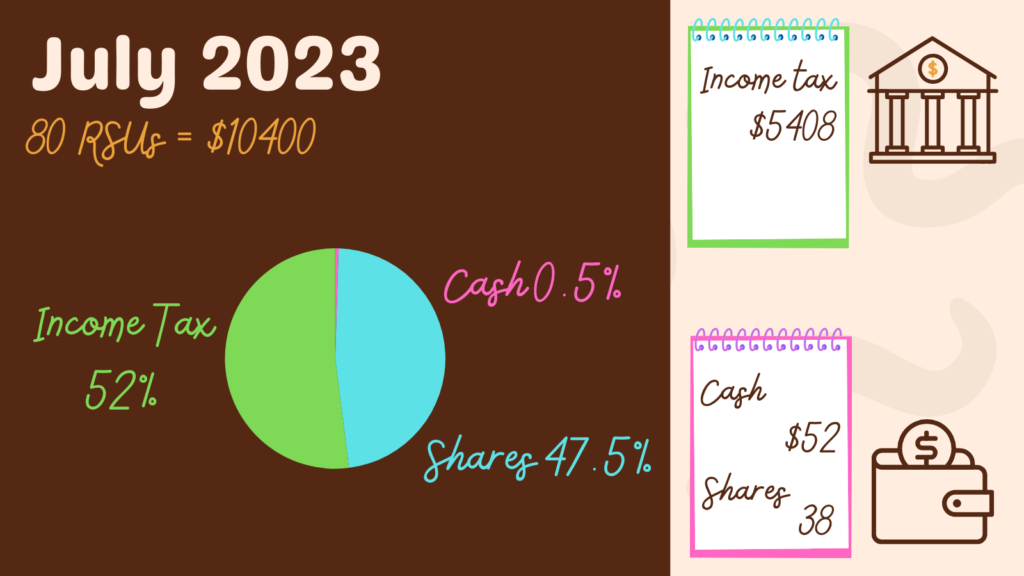

July 2023: 4 (=80) RSUs, share value: $130

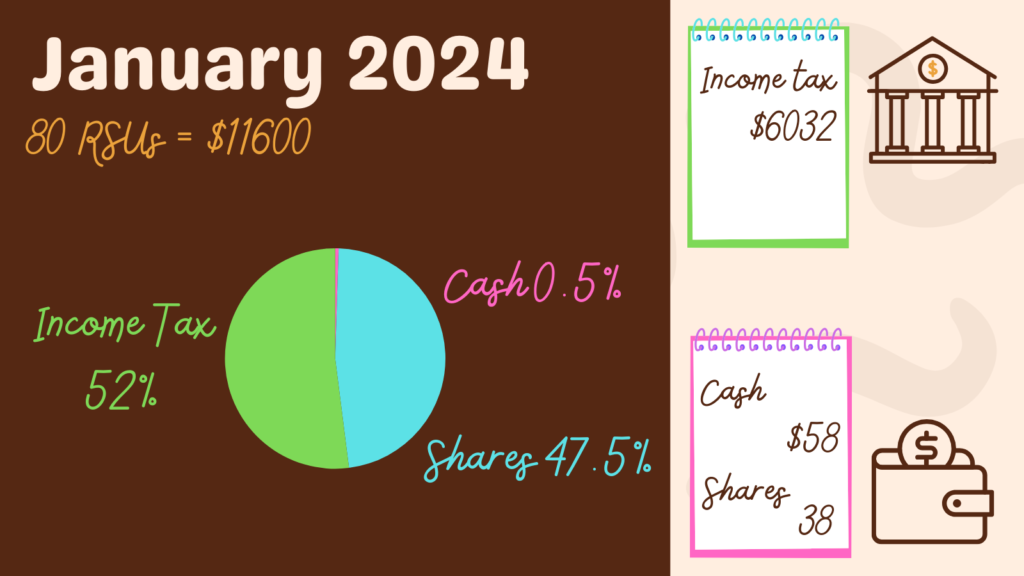

January 2024: 4 (=80) RSUs, share value: $145

January 2025: ------, share value: $234 <- value when selling

Pull Out Your Calculators!

Each vesting has its calculation — different share values, different tax amounts to pay, and different shares left post-taxes. There are three cases I’d like to go over:

- Vesting (pre-split) where tax requires selling all shares.

- Vesting (pre-split) with shares left post taxes.

- Vesting post-split.

Lucky for us, these are the first three vestings (January 2021, January 2022, and July 2022). I will cover those scenarios within the blog post, and the rest of the calculation slides I’ll attach at the end of the blog post.

Lastly, we will calculate the profit if Aoife were to sell all her shares in 2025.

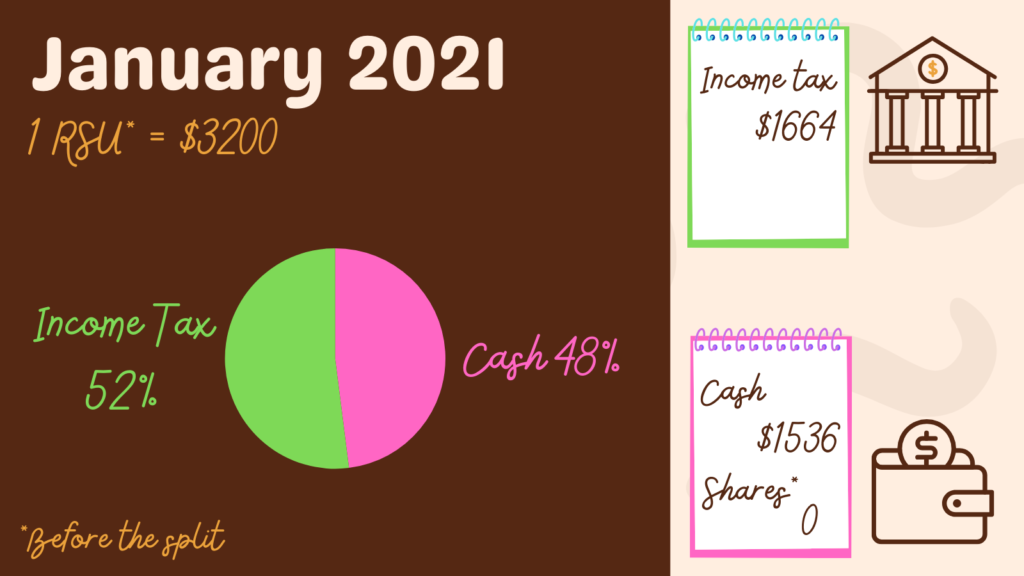

1. January 2021 — A Single Share Vesting

Here we have 1 (pre-split) RSU, with a value of 160*20= $3200. Taxes for this income are 3200*0.52= $1664. Because Aoife is selling-to-cover + there is only 1 share = she sells the share and gets an extra 3200*0.48= $1536 in her next paycheck. By the way, she will also see a line in the deduction column named “RSU TX WH” — which indicates money withholding for taxes from that vesting.

Note that when Aoife logs into her brokerage account, she will see that out of 20 shares vested in January 2021 — all were sold, which doesn’t fit the sell-to-cover approach. If it was, she would’ve sold only 11 shares and get to keep 8. This mismatch is because the number of shares presented is post-split, while the vesting was pre-split. Very confusing, I know!

Let’s review the other options for vesting on this example:

- Selling for profit: In this case, sell-for-profit = sell-to-cover, because there was only one share.

- Paying tax in advance: In that case, Aoife would’ve paid $1664 before the vesting, and then instead of getting $1536, she would’ve received 1 share.

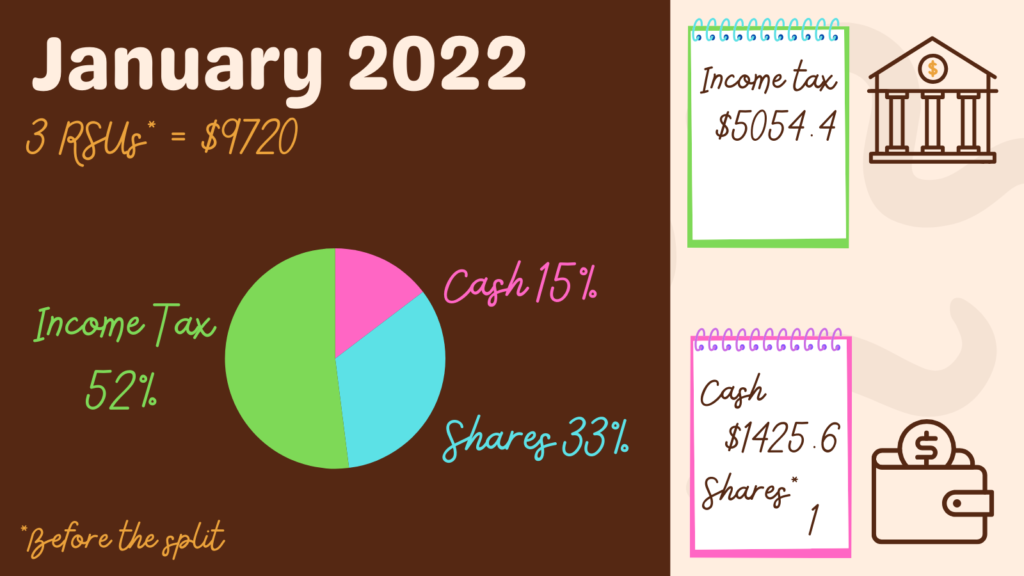

2. January 2022 — A Pre-Split Vesting

Here we are still with the old shares. The value of the income (the granted 3 stocks) is 3*20*162= $9720. Therefore, income tax is 9720*0.52= $5054.4. Because Aoife is selling-to-cover, she has to sell 2/3 of her shares: This gives her 2*20*162=$6480. Lastly, after covering taxes, she is left with 6480-5054.4= $1425.6 extra cash in her next payslip.

To conclude, in January 2022, Aoife gets 1 share (pre-split, worth $3240) and $1425.6 cash.

Here as well, when Aoife logs into her brokerage account, she will see that out of the 80 shares she received in January 2022 — 60 were sold, which doesn’t fit the sell-to-cover approach. If it was, she would’ve sold only 42 shares and get to keep 38. This mismatch is because the number of shares presented is post-split, while the vesting was pre-split.

Let’s review the other options of vesting on this example (just to ensure we understand!):

- Sell-for-profit: In this case, Aoife would’ve gotten

9720 * 0.48 =$4665.6 and 0 shares. - Paying tax in advance: In that case, Aoife would’ve needed to pay $5054.4 from her own money, and then she would’ve gained 3 shares.

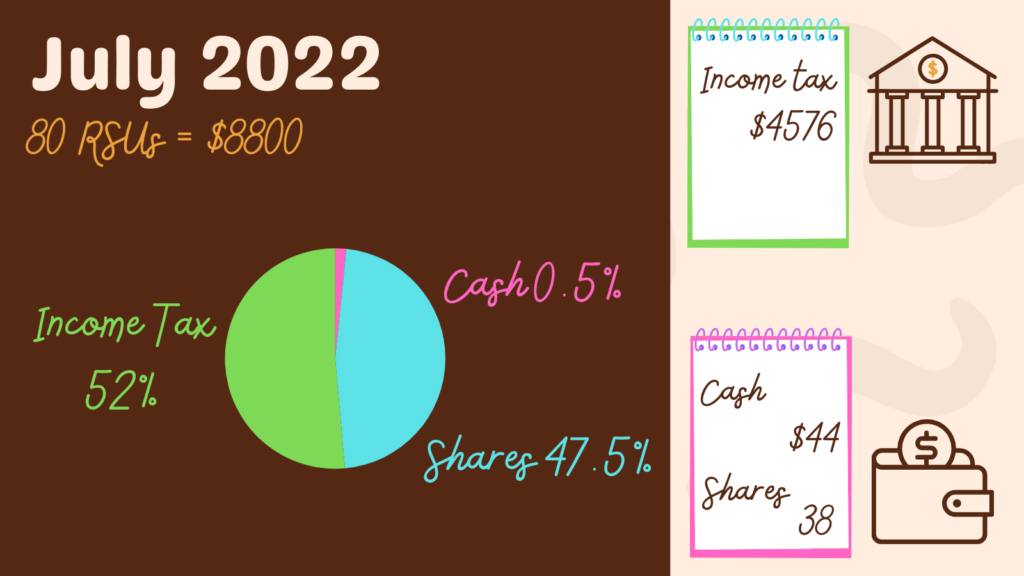

3. July 2022— A Post-Split Vesting

This is the first vesting post-split! Originally Aoife was granted 4 RSUs with the original value, but after the split, those 4 shares became 80 shares, with the total value remaining the same: 80*110= $8800.

With smaller shares, we can sell-to-cover taxes more accurately — leaving us with more shares and less cash: Taxes for this income are 8800*0.52= $4576. To cover taxes, Aoife needs to sell 4576/110=41.6 -> 42 shares. Therefore, out of the 80 shares — Aoife keeps 38 shares, pays $4576 tax, and gets 42*110-4576= $44 extra cash in her next paycheck.

This was the calculation of the third vesting out of six. You can find the calculation slides for the rest of the vestings in the appendix of the blog post.

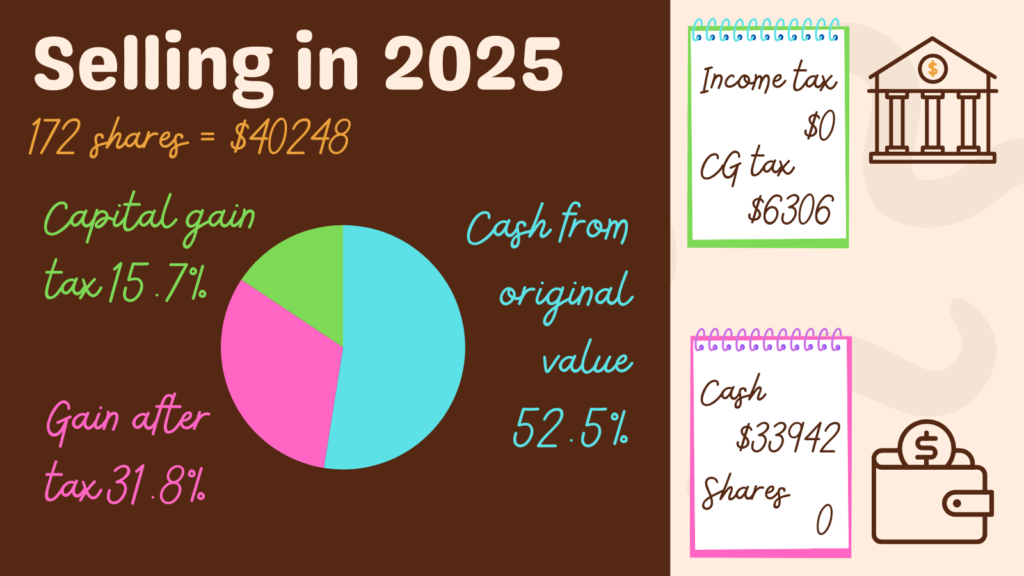

4. January 2025 — Selling All Shares

Ok, now Aoife wants to sell her stocks! She checked the current share value, and was happy to see that it increased since her RSUs vested! But… how much cash will she get? Let’s calculate!

For each vesting period, we need to calculate the difference between the total shares value on vesting and at the time of selling ($234 at the time of writing). That difference is the profit — and Aoife needs to pay capital gain tax on that.

Note that there are only 5 vestings in the image above, but there were 6 vesting dates. That is because the first vesting (January 2021) didn’t result in any shares.

Let’s look at the numbers: Aoife accumulated 172 shares that at the time of selling are worth 172*234= $40248. Out of that, 3240+4180+3268+4940+5510= $21138 is income Aoife already paid tax on because that was the value at the time of vesting. That’s what I call “Cash from original value”. The profit from the shares invested is 40248-21138= $19110. This amount is the capital gain — which requires a tax of 19110*0.33= $6306 (I rounded down), leaving us with 19110-63006= $12804.

Therefore, the total amount of cash entering Aoife’s account is 21138+12804= $33942.

To Conclude

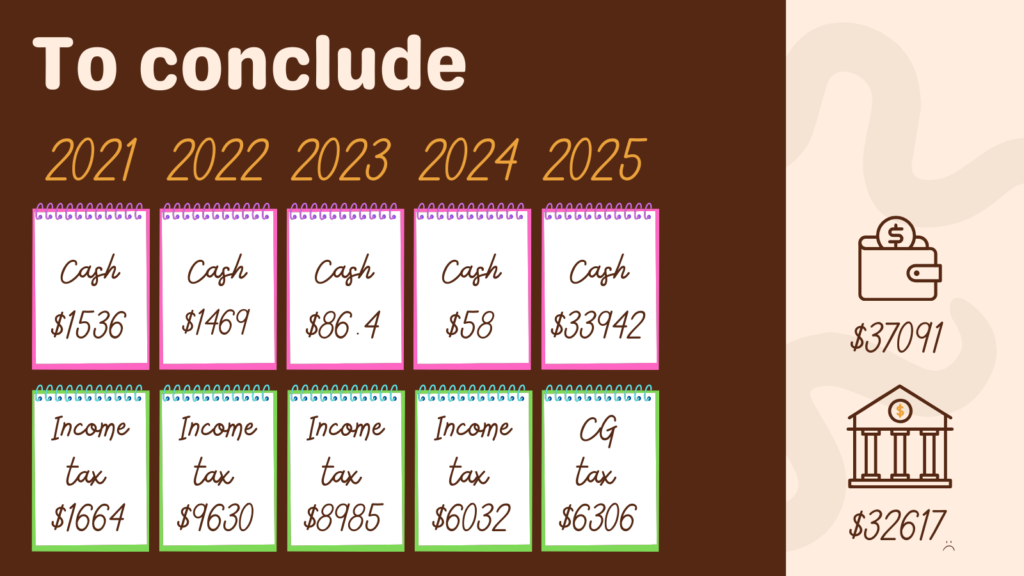

Now, we can take all the cash earned over all the years, and sum it up:

Now, Aoife is wondering what would the profit be if she were to choose another vesting option:

- Sell-all is easy to calculate: the value of shares vested * 0.48 (assuming 52% taxes). This means there is no income in 2025.

- Keep-all calculation: keep the original number of shares vested, and extract the cash paid to cover taxes from the gain made in 2025.

Note that in Aoife’s case, if she were to not invest the cash in anything else in the “sell-all” option, and if Nile’s share value goes as in the example: keep all would’ve been the most profitable option.

Buying shares is a gamble because you don’t know if they will go up or down when you need to cash them out. Therefore, there is no “best approach” with your RSUs: Do what fits you, your financial situation, and your comfort (enjoyment?) with risk-taking.

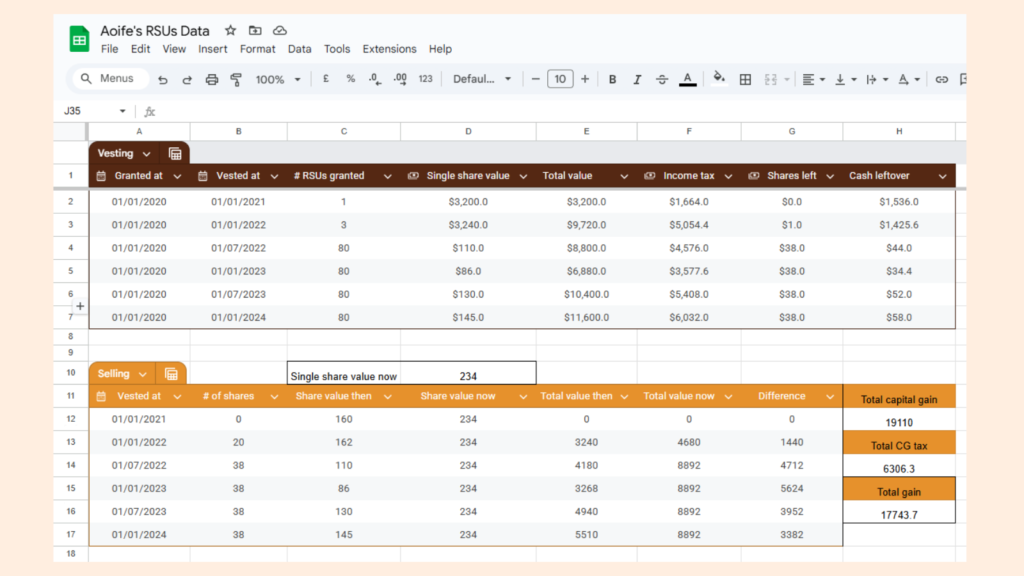

For your convenience, I created a Google sheet with Aoife’s RSU calculations: you can make a copy and put your numbers in!

That’s it for today! Interested in digging more into your paycheck? Check out my blog post about Turning PDF Payslips Into a Single CSV Report!

Appendix

The slides for the rest of the vesting calculations: